Claim adjudication, the process of determining the financial liability of a claim by the insurance company, is quite complex and time-consuming. Adjudication can be quick if the received claim is clear to the dot, in the sense that all the information is accurate and the claim is within the limits of the policy. But, as with all things in life, this is never the case.

The challenge lies in verifying the correctness and authenticity of the filled information. The amount of money spent by the insurance company in verifying claims impacts the bottom line and finds mention as loss adjusted expense (LAE) in the financial reports. Delays in claim verification and settlement can also cause customer dissatisfaction, which in today’s competitive landscape, no insurer can afford to ignore. By embracing automation, the insurance industry can turn these around and set new standards in claims adjudication and settlement.

According to the Council for Affordable Quality (CAQH) Index report, automating eligibility and claim verification can lead to an annual saving of $ 5.2 billion in healthcare insurance alone. Let me explain how AI and machine learning can be effectively used to automate the claim adjudication process, minimize the loss adjusted expense, and enhance customer experience.

Understanding the Claim Adjudication Process

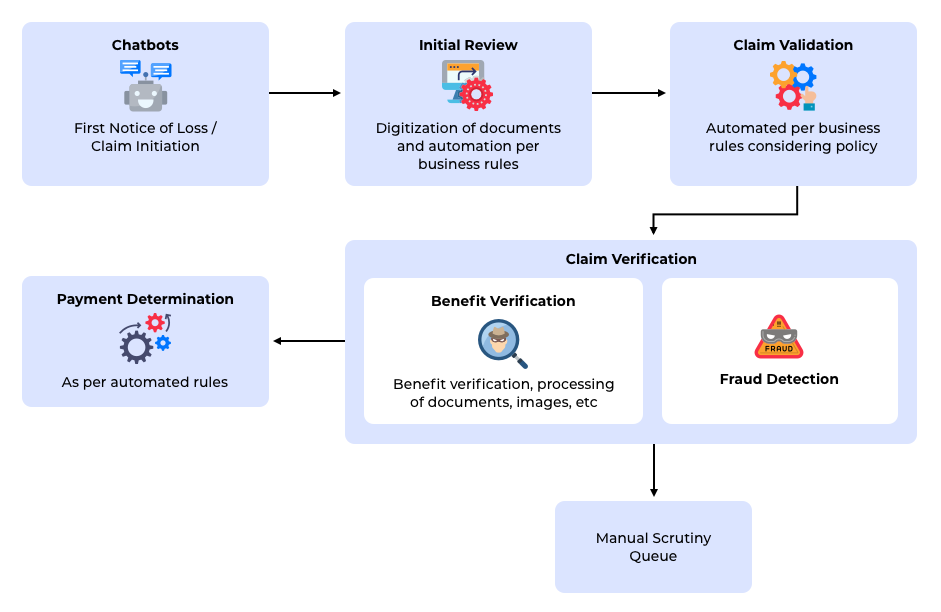

The claim adjudication process starts with the requester initiating the first notice of loss (FNOL). This is just a fancy term for the first notification to the insurance provider after the insured asset’s loss, theft, or injury. After the first notice of loss, there is an initial review to check simple errors or omissions. Ther review can be through an automated or manual process depending on the sophistication of the insurance provider. Examples of such errors are wrong or invalid customer identifiers, mismatched service type and patient details, etc. These are generally errors that can be captured by simply matching the electronic record of claim requests and customer records.

After this review, the claim request goes through a second review process that involves more complex verification steps like eligibility and benefit verification, coordination of benefit in case multiple insurance providers are involved, etc. The third stage is a manual review process that is executed by domain experts like medical practitioners in case of health care claims or automobile accident surveyors in case of automobile claims. Additional information or supporting documents may be requested at this stage. The next step in the flow is the payment determination process to finalize the amount to be paid to the customer. The outcome of this process is either a complete approval or a reduced payout or a denial of the claim. The last step, payment determination, is usually done based on well-defined business rules and mathematical formula. Hence there is very little room for ambiguity in this process.

Claim Initiation and Validation

Automating the claim initiation process saves insurers considerable time. It is best done by using a chatbot that can interact with customers and collect the required information. The advantage of using a chatbot is that information can be captured in a structured form and a first-level validation can be carried out during the claim initiation process. A chatbot can access customer information on the fly and prompt the user for details or additional information in case something does not match up. Another possible automated validation is the prevention of duplicate claims. If all the information pertaining to claims is digitized, it is possible to reject or scrutinize a possible duplicate claim very early in the processing cycle. Using a chatbot for claim initiation can reduce delays in reverting to customers for additional information or corrections. Building such a chatbot is not an easy game and requires elaborate framework development. QBurst has developed a reusable chatbot framework and architecture that can be customized for various domains.

That said, it is possible that tight coupling with legacy processes may prevent organizations from adopting a completely chatbot-based claim initiation process. In that case, a middle ground between the manual paper-based process and the chatbot can be found in the automated processing of claim forms. QBurst's reusable components in retrieving information from printed and handwritten forms can help you implement this strategy in very little time.

Claim Verification

Traditionally, claim verification is done through well-defined manual processes. Verifying the authenticity of the claim requires scrutinizing the basic details of the claims and the supporting documents. In case the amount is higher than a threshold, it is marked for advanced scrutiny and sent to approvers higher in the hierarchy. At times, even for claims that lie well within their approving limits, approving officers may classify a claim as possible fraud or set it aside for advanced scrutiny. Advanced scrutiny of the claim often requires contributions from domain experts.

Automating the role of first-level officers is possible with the current advanced machine learning capabilities. First-level approvers often carry out their tasks based on well-defined rules. The catch here is that, before applying their rules, these officers often have to read through pages of information and images. Advances in the area of computer vision and natural language processing allow us to automate this information extraction process. For example, extracting information from lab reports can be done by a combination of object detection algorithms, optical character recognition, and natural language processing. Watch this space for a detailed blog post on the architecture behind such information extraction and how it can be accomplished. Similarly, advanced vision algorithms can be used in the auto industry too to decide whether to repair, replace, or push for a total loss claim based on images. Once the information is accurately extracted, applying the business rules on them can easily be automated.

The final step in the claim verification process is to automate the decision to push a claim for advanced scrutiny. This can be done using a classification model built based on historical insurance claim data. While most basic features can be modeled using statistical techniques, neural network models will allow you to consider natural language-based and image-based features too (Typical ML models for fraud detection and the challenges in building them are discussed here).

The output of the collection of models and engines that verify the claim will be an approval, rejection, or a reduced payout. Claims that fit well with the business rules for triggering the advanced scrutiny and successfully pass the fraud detection models can be pushed directly for payout determination without manual intervention at all. Other claims can be routed to the advanced scrutiny process that involves manual intervention.

Conclusion

Machine learning in claim adjudication is not about creating a model that provides a yes or a no answer but automating multiple steps using different models and then integrating them all together to arrive at the final payout value or approval. Applying machine learning in such a complicated process requires domain expertise as well as skills in multiple areas like image processing, natural language processing, and statistical number crunching. The impact of AI on pricing, risk selection, and assessment, customer engagement is already beginning to show. The technology to modernize the insurance industry is there. What's required is the commitment from insurers to take it to the next level by implementing an automated insurance pipeline that can boost insurance performance and elevate customer experience.